Article 1 – Let’s Understand the Meaning of each word

For the purposes of this Decree-Law, the following terms are defined as follows, unless otherwise indicated by the context:

- State: United Arab Emirates.

- Federal Government: The government of the United Arab Emirates.

- Local Government: The government of any of the UAE’s Member Emirates.

- Ministry: Ministry of Finance.

- Minister: Minister of Finance.

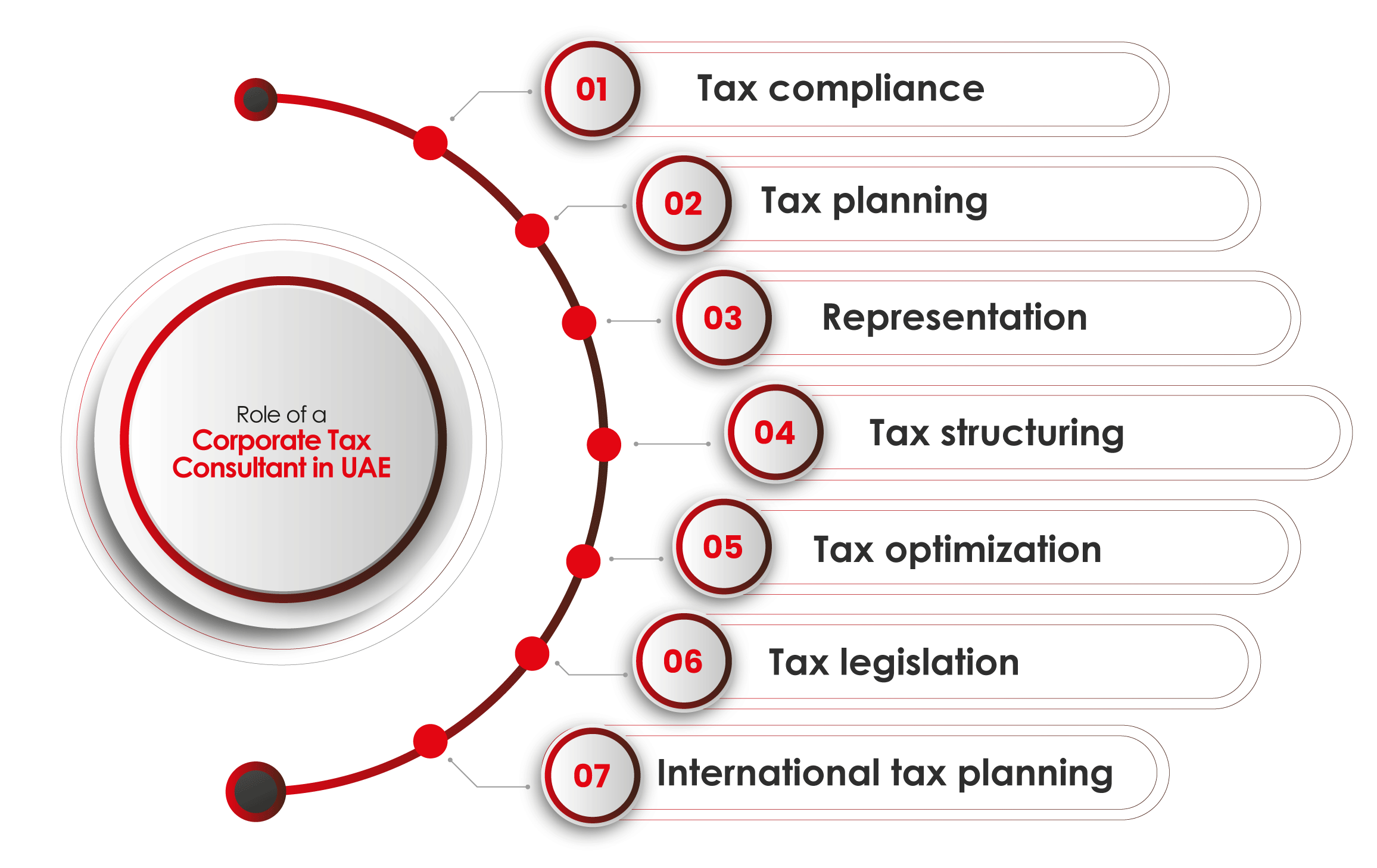

- Authority: Federal Tax Authority.

- Corporate Tax: Tax imposed on juridical persons and Business income by this Decree-Law.

- Business: Any ongoing and independent activity conducted in any location, including industrial, commercial, agricultural, vocational, professional, service, excavation, or other activities related to tangible or intangible properties.

- Qualifying Income: Income earned by a Qualifying Free Zone Person, subject to the Corporate Tax rate per Clause 2(a) of Article 3.

- Government Entity: Federal or Local Governments, ministries, departments, agencies, authorities, and public institutions.

- Government-Controlled Entity: A juridical person wholly owned and controlled by a Government Entity, as specified by Cabinet decision.

- Person: A natural or juridical person.

- Business Activity: Any transaction or series of transactions conducted by a Person within their Business operations.

- Mandated Activity: Activities conducted by a Government-Controlled Entity as established by legal mandate, specified by Cabinet decision.

- State’s Territory: Includes UAE lands, territorial sea, and airspace.

- Natural Resources: Non-renewable, non-living resources, such as water, oil, gas, coal, and naturally formed minerals.

- Extractive Business: Activities involving exploration, extraction, or exploitation of the State’s Natural Resources.

- Non-Extractive Natural Resource Business: Activities related to treating, processing, or distributing the State’s Natural Resources.

- Qualifying Public Benefit Entity: Entity meeting the conditions in Article 9 and listed in a Cabinet decision.

- Qualifying Investment Fund: Entity that raises or pools funds for investment purposes as per Article 10.

- Exempt Person: A Person exempt from Corporate Tax per Article 4.

- Taxable Person: A Person subject to Corporate Tax in the UAE under this Decree-Law.

- Licensing Authority: Competent authority for licensing Businesses in the UAE.

- Licence: Document from the Licensing Authority allowing Business operations.

- Taxable Income: Income subject to Corporate Tax under this Decree-Law.

- Financial Year: Period as defined in Article 57.

- Tax Return: Information filed with the Authority for Corporate Tax purposes.

- Tax Period: Duration covered by the Tax Return.

- Related Party: Person associated with a Taxable Person as per Article 35(1).

- Revenue: Gross income during a Tax Period.

- Recognised Stock Exchange: Licensed stock exchange within or outside the UAE.

- Resident Person: Taxable Person defined in Article 11(3).

- Non-Resident Person: Taxable Person defined in Article 11(4).

- Free Zone: Designated geographic area within the UAE, per Cabinet decision.

- Free Zone Person: Juridical person registered in a Free Zone, including branches of Non-Resident Persons.

- Unincorporated Partnership: Contract-based relationship between two or more Persons.

- Permanent Establishment: Business presence in the UAE of a Non-Resident Person, per Article 14.

- State Sourced Income: Income from the UAE as specified in Article 13.

- Qualifying Free Zone Person: Free Zone Person meeting Article 18 conditions.

- Investment Manager: Licensed provider of investment services.

- Corporate Tax Payable: Due Corporate Tax for one or more Tax Periods.

- Foreign Partnership: Contract-based association of two or more Persons in a foreign jurisdiction.

- Foreign Tax Credit: Deductible foreign tax, per Article 47(2).

- Family Foundation: Foundation or similar entity as defined in Article 17.

- Interest: Payment for the use of money or credit, excluding principal amounts.

- Accounting Income: Net profit or loss per financial statements, as per Article 20.

- Exempt Income: Corporate Tax-exempt income under this Decree-Law.

- Connected Person: Affiliated Person as per Article 36(2).

- Tax Loss: Negative Taxable Income for a Tax Period.

- Qualifying Business Activity: Activity specified by Cabinet decision.

- Foreign Permanent Establishment: Business presence outside the UAE for a Resident Person, as per Article 14.

- Market Value: Price in an arm’s-length free-market transaction.

- Qualifying Group: Taxable Persons meeting conditions in Article 26(2).

- Net Interest Expenditure: Interest expenditure exceeding Interest income under this Decree-Law.

- Bank: Licensed financial institution as defined in UAE legislation.

- Insurance Provider: Licensed entity accepting insurance risks.

- Control: Direction or influence over one Person by another per Article 35(2).

- Tax Group: Taxable Persons treated as a single Taxable Person under Article 40.

- Withholding Tax Credit: Deductible withholding tax per Article 46(2).

- Withholding Tax: Corporate Tax on State Sourced Income per Article 45.

- Tax Registration: Corporate Tax registration with the Authority.

- Tax Registration Number: Unique number issued by the Authority.

- Tax Deregistration: Corporate Tax deregistration with the Authority.

- Tax Procedures Law: Federal law governing UAE tax procedures.

- Administrative Penalties: Penalties imposed under this Decree-Law or the Tax Procedures Law.